Published in Market Analysis

EU Meat Prices Hold Firm in March 2026

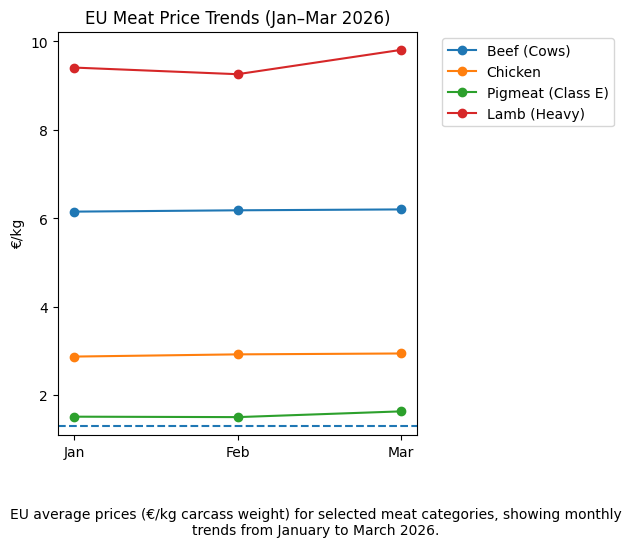

EU meat prices remained elevated in March 2026, with beef and lamb holding peak levels while pigmeat and poultry showed early signs of stabilisation.

Martina Osmak

Director of Marketing

Introduction

March 2026 confirms what the market has been signaling since late 2025: European meat prices are not easing. Despite expectations of seasonal corrections, most categories remained at historically high levels, with only minor shifts compared to January and February.

This report analyses March 2026 EU meat prices across key categories, using official market data converted into €/kg carcass weight. It also compares movements over the first quarter of 2026 to highlight whether prices are still rising, stabilising, or beginning to soften.

Key Takeaways at a Glance

Meat prices remain structurally high, with no meaningful correction in Q1 2026

Beef prices are stable at peak levels, not rising further but not falling either

Lamb continues to be the most expensive and volatile category

Pigmeat shows early signs of stabilisation, though still uneven across countries

Chicken remains the cheapest protein, with relatively small monthly movement

Large price gaps between countries persist across all categories

Quarter Comparison (Jan → Feb → Mar 2026)

Beef: Peaked in 2025 → stabilised across Q1 2026

Lamb: Stayed extremely high → slight upward pressure in March

Pigmeat: Volatile in January/February → more stable in March

Chicken: Mostly flat → minor fluctuations only

Piglets: Still highly volatile → strong country divergence remains

Category Breakdown – March 2026 (€/kg)

Chicken

EU average: €2.94/kg

Lowest: Poland (€2.00/kg)

Highest: Germany (€4.60/kg)

Chicken prices remained broadly stable compared to February. The category continues to act as a price anchor in the protein market, benefiting from lower production costs and strong substitution demand.

Trend vs Jan–Feb:

Chicken prices remained stable with a slight upward trend across Q1 2026.

After a small increase from January to February, prices continued to edge up in March, showing consistent but modest growth.

Interpretation:

Chicken continues to behave as a cost-stable protein, with gradual increases likely linked to feed and energy costs rather than supply shortages. It remains the most predictable category.

Cows (Beef)

EU average: €6.20/kg

Lowest: Slovenia (€4.70/kg)

Highest: Sweden (€7.59/kg)

Cow prices increased slightly from February, confirming continued tight supply. The market shows no sign of easing, with Northern Europe still commanding premium prices.

Trend vs Jan–Feb:

Cow prices showed very limited movement, increasing slightly across the three months.

The trend is almost flat, with only marginal upward pressure.

Interpretation:

This confirms a tight but stable supply situation. The market is not accelerating further, but high price levels are being maintained due to limited availability.

Heifers (Beef)

EU average: €7.33/kg

Lowest: Hungary (€4.33/kg)

Highest: Italy (€8.17/kg)

Heifer prices edged higher again in March, reinforcing the structural shortage of slaughter-ready animals.

Trend vs Jan–Feb:

Heifer prices remained high and mostly stable, with a slight increase into March.

Interpretation:

This reflects continued herd retention behavior farmers are still holding back animals for breeding, which limits supply but does not create sharp monthly price jumps.

Male Bovines (Beef)

EU average: €7.18/kg

Lowest: Denmark (€6.12/kg)

Highest: Sweden (€8.10/kg)

Prices remained stable, with very limited movement. This category continues to reflect overall beef market tightness rather than volatility.

Trend vs Jan–Feb:

Stable

Steers (Beef)

EU average: €7.07/kg

Lowest: Romania (€5.38/kg)

Highest: Sweden (€8.15/kg)

Steer prices show slight softening compared to February but remain historically high.

Trend vs Jan–Feb:

Slight stabilisation

Young Bovines (Beef)

EU average: €7.26/kg

Lowest: Latvia (€5.16/kg)

Highest: Sweden (€8.02/kg)

Young bovine prices remained firm, with strong price concentration in higher-value markets.

Trend vs Jan–Feb:

Stable

Young Bulls (Beef)

EU average: €7.28/kg

Lowest: Denmark (€6.12/kg)

Highest: Sweden (€8.10/kg)

Very limited change month-to-month. The category shows clear price plateauing.

Trend vs Jan–Feb:

Stable

Across all major beef categories, prices show a consistent pattern:

Small fluctuations month-to-month

Slight upward movement into March

No sharp spikes

Interpretation:

The beef market is structurally tight but no longer accelerating.

Prices are holding at high levels rather than rising rapidly - a sign of market stabilisation at elevated levels, not decline.

Lamb – Heavy

EU average: €9.81/kg

Lowest: Finland (€6.10/kg)

Highest: Croatia (€13.63/kg)

Heavy lamb prices increased further in March, reinforcing the category as the tightest supply market in the EU.

Trend vs Jan–Feb:

Increasing

Lamb – Light

EU average: €9.83/kg

Lowest: Latvia (€7.08/kg)

Highest: Croatia (€13.60/kg)

Light lamb continues to mirror heavy lamb dynamics, with extremely high top-end prices.

Trend vs Jan–Feb:

Stable to slightly rising

Lamb prices show the clearest upward movement among all categories:

Slight dip or stability in February

Strong rebound in March

Interpretation:

This reflects seasonal demand effects combined with very limited supply.

Lamb remains the most supply-constrained and reactive market, which is why it shows the strongest price movements.

Piglets

EU average: €0.61/kg

Lowest: France (€0.44/kg)

Highest: Sweden (€1.05/kg)

Piglet prices rose compared to February, showing renewed farmer demand and expectations of future pig profitability.

Trend vs Jan–Feb:

Piglet prices show clear volatility with an upward move into March:

Flat/slight dip in February

Noticeable increase in March

Interpretation:

This confirms that piglets are not stable - they react strongly to farmer expectations and restocking cycles.

March likely reflects renewed confidence or preparation for future production.

Pigmeat – Class E

EU average: €1.63/kg

Lowest: Netherlands (€1.27/kg)

Highest: Sweden (€2.57/kg)

Class E prices increased slightly, suggesting the pig sector may be entering a more balanced phase.

Trend vs Jan–Feb:

Pigmeat prices show a flat-to-rising pattern:

Stable between January and February

Clear increase in March

Interpretation:

Rather than fully stabilising, the market is moving sideways with short-term upward pressure.

This suggests:

Supply is still constrained

Demand may be recovering slightly

Pigmeat – Class R

EU average: €1.84/kg

Lowest: Czechia (€1.34/kg)

Highest: Italy (€1.91/kg)

Prices remained stable with limited dispersion changes.

Trend vs Jan–Feb:

Stable

Pigmeat – Class S

EU average: €1.63/kg

Lowest: Netherlands (€1.28/kg)

Highest: Sweden (€2.62/kg)

Class S continues to show strong country divergence but no major shift in trend.

Trend vs Jan–Feb:

Stable

Both categories (R&S) follow a similar pattern:

Limited movement early in the year

Gradual increase into March

Interpretation:

Pigmeat markets are less volatile than piglets but not fully stable.

They show mild upward adjustment, likely reflecting cost pressures and tightening supply rather than demand spikes.

What Changed in March (vs Jan & Feb)

1. Beef: Plateau, not decline

Beef prices are no longer rising - but importantly, they are not falling either. This indicates:

Continued tight supply

No strong demand destruction yet

Market reaching a temporary ceiling

2. Lamb: Still tightening

Lamb prices pushed higher again, especially in:

Croatia

Southern/Eastern EU

This confirms:

Structural supply shortage

Strong seasonal demand building

3. Pigmeat: Early stabilisation

After volatility in early 2026:

Prices are now more consistent across months

Piglet prices rising → signal of future supply expectations

4. Chicken: Stability leader

Chicken remains:

Predictable

Affordable

Less exposed to supply shocks

Conclusion

March 2026 confirms that EU meat markets are not correcting downward after the highs of 2025. Instead, prices are stabilising at elevated levels, especially in beef and lamb.

The most important shift is not price direction -but price persistence. High prices are no longer temporary-they are becoming the new baseline.

Pigmeat may be the first category to stabilise structurally, while lamb remains the most supply-constrained and volatile market in the EU.

Source: https://agridata.ec.europa.eu/extensions/DataPortal/prices.html